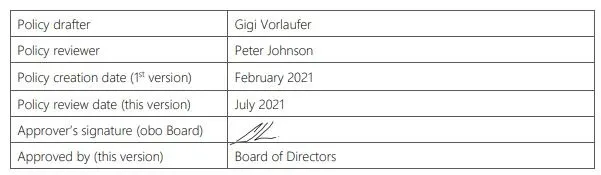

1. Policy approval and information

2. Purpose and scope

Treating Customers Fairly (TCF) forms part of the market conduct framework being implemented by the Financial Sector Conduct Authority (the Authority), being the market conduct regulator of the financial services industry in South Africa. The TCF consumer protection framework (TCF framework) is applicable to all South African regulated financial institutions, including, but not limited to Authorised Financial Services Providers (FSPs), licensed under the Financial Advisory and Intermediary Services Act 37 of 2002 (the FAIS Act), retirement funds, and their administrators, licensed under the Pension Funds Act 24 of 1956 (the PFA), insurers licensed under the Insurance Act 18 of 2017 (re-licensing process in progress), and managers of collective investment schemes, licensed under the Collective Investment Schemes Control Act 45 of 2002, all through the Financial Sector Regulation Act 9 of 2017 (the FSRA).

The Company strives to apply the highest standards of ethical behaviour during the conduct of its business activities, and this behaviour is expected of all its employees and associates. The Company always aims to act in the best interest of customers, and in this regard, the Policy is intended to provide for the fair treatment of customers (including potential customers).

The Company is committed to the TCF outcomes, which are the results, or consequences, which customers should experience when fair business practice is consistently applied, and is embedding this culture into the business, by ensuring that:

2.1. Outcome 1: Customers can be confident they are dealing with a company where TCF is central to the corporate culture.

2.2. Outcome 2: Financial Products and Services, marketed and sold, are designed to meet the needs of identified client groups, and are targeted accordingly.

2.3. Outcome 3: Customers are provided with clear information, and are kept appropriately informed, before, during, and after, the point of sale.

2.4. Outcome 4: Where financial advice is given, it is suitable, and takes account of client circumstances.

2.5. Outcome 5: Financial products perform as the Company has led customers to expect, and service is of an acceptable standard, and is as customers have been led to expect.

2.6. Outcome 6: Customers do not face unreasonable post-sale barriers imposed by the Company, to change financial products, switch product suppliers, switch financial services providers, submit a claim, or make a complaint.

The Policy formalises the TCF standards applied by the Company, in accordance with the TCF framework, to enhance the business focus on customers. The Company applies the TCF principles across its strategies, people, policies, processes, and systems, which are related to, where applicable, product development, marketing, sales, providing advice, communications, service, administration, and complaints management. The Company tries to ensure fair business practice, to consistently deliver fair outcomes for customers.

This policy provides controls, to reduce the probability of the below risks occurring:

- Customers may become dissatisfied and alienated, due to the Company’s failure to treat them fairly, and in accordance with what the Company has led those customers to believe.

- The reputation of the Company may be negatively impacted, due to non-compliance with the TCF principles.

- Failure to comply with the TCF principles may result in closer supervision by the Authority.

- Regulatory sanctions may be imposed by the Authority, due to failure to deliver on any of the TCF outcomes.

This Policy considers the market conduct framework being implemented by the Authority, including all publications relating to TCF. It also considers the principles embodied by the Companies Act 71 of 2008 and the King Code of Governance for South Africa 2009 (King IV).

This policy is applicable to all employees of the Company and its subsidiaries, and all relationships with Third Parties.

3. Definitions

3.1. Company means SCM DMA (Pty) Ltd.

3.2. Authority, or FSCA, means the Financial Sector Conduct Authority, being the market conduct regulator.

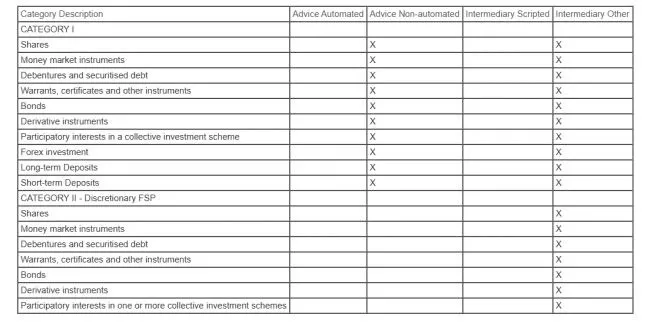

3.3. Financial Products and Services, offered by the Company (delete those that are not applicable),

means the list of financial products and services reflected in Annexure A of this policy.

3.4. TCF Champion means the person responsible for implementing, and maintaining, the TCF standards within the Company as set out in 11.1.

3.5. Third Party means product suppliers, product distributors, and service providers, with whom we have agreements in place, forming part of the value chain of the offerings that we provide our customers. Some third parties are financial institutions that are required to comply with the TCF framework. Regardless of whether, or not, third parties are financial institutions, we are responsible to reasonably interact with third parties.

4. Roles and responsibilities

4.1. Board of directors (board) maintains overall responsibility for the Policy, which may be delegated to the relevant stakeholders for implementation.

4.2. Executive committee (Exco) is the most senior management team within the Company. It is responsible for drafting and implementing this Policy, and for submitting it to the Board of directors for approval, through the Audit Committee, being a sub-committee of the Board of directors. It must ensure that all employees and associates are aware of the Policy, and understand the contents thereof, and provide training and awareness to facilitate this. The Exco may delegate the implementation thereof to line management.

4.3. Governance structure

The Company must have governance structures in place, to ensure compliance with this Policy. The Audit Committee must have an overview of the general and specific compliance requirements.

4.4. Internal audit, in its capacity as the third line of defence, provide assurance over this Policy, by providing an independent assessment of the adequacy and effectiveness of the overall risk management framework and risk governance structures, through the annual risk-based audit plan. Internal audit has the authority to independently determine the scope and extent of work to be performed, as mandated by the Audit Committee.

4.5. Compliance officers must monitor compliance with this Policy, and report non-compliance to the Exco and the governance structures. They must provide guidance and training to employees, to assist them in understanding the Policy and their obligations thereto.

4.6. Employees must ensure that they understand this Policy, and always comply with it. They must continuously assess their own environment, to ensure the fair treatment of customers, and take the appropriate course of action, in terms of the Policy. Employees must be cognisant of the consequences of non-compliance with the Policy.

5. Outcome 1: corporate culture

5.1. The Company is confident that it provides financial services where the fair treatment of its customers is central to its corporate culture. Customer satisfaction should not be misconstrued for fairness. If a client is satisfied with the service provided, it does not necessarily mean that the Company has treated the customer fairly. We are committed to ensuring that all our customers can be confident they are dealing with a company where TCF is central to the corporate culture.

5.2. The Company aims to ensure that its employees, including its representatives, provide financial services honestly, fairly, with due skill, care and diligence, and in the interests of customers and the integrity of the financial services industry.

5.3. Delivering the TCF outcomes is embedded within the Company’s corporate culture, including its values, code of conduct, ethics policy and structure.

5.4. Procedures implemented to achieve Outcome 1:

- Leadership

- The Company ensures that its Exco fully understands the TCF objectives and is held accountable.

- Exco has adopted TCF deliverables, has been allocated specific responsibilities, and those who contribute to providing financial service, understand their respective TCF roles.

- Exco conducts regular reviews of the main business processes to identify areas that do, or may, require improved TCF deliverables. Explicit provision has been made to consider TCF implications and deliverables during the strategic planning process of any new strategy, or change in existing strategy.

- Decision making

- New initiatives must clearly indicate that the TCF implications have been considered.

- The Company has mechanisms through which employees can debate TCF related matters, and refer questions, or concerns, to the TCF Champion.

- Governance and controls

- Employees report progress made in achieving TCF deliverables within their business areas to Exco through the relevant structure.

- The risk management framework takes market conduct risks, including TCF, into consideration, which is monitored and supervised by the board.

- As part of approving new business cases or projects, the TCF implications must have been considered.

- Employee participation

- The business roles have been identified which require the delivery of TCF outcomes.

- Employees receive training to ensure they understand the TCF principles and deliverables relating to their roles, and in general.

- Employees understand their respective TCF responsibilities. This Policy has been circulated to employees who are encouraged to make suggestions to the TCF Champion about how TCF may be improved.

- Performance management

- Line managers must assess employees’ adherence to their TCF responsibilities, as part of the formal performance management process.

- Management information

- TCF related information is gathered and analysed regularly to improve the Company’s adherence to the TCF outcomes.

- Information that is gathered, is used as part of the TCF monitoring process.

- Information is provided to the board and Exco, assisting them to assess the Company’s adherence to the TCF outcomes.

- Information is provided to the Authority, as may be required, or requested.

- The Company monitors and responds to changes in the broader environment such as economic and regulatory developments, to enable the Company to proactively identify TCF related risks and react to those risks as soon as reasonably possible.

6. Outcome 2: Financial Products and Services

6.1. The Financial Products and Services offered by the Company are designed to meet the needs of customers; are marketed in an appropriate way that considers the type and circumstances of customers; provide value for money for customers; consider the risk profile of customers; and, are understandable and easily accessible.

6.2. Procedures implemented to achieve Outcome 2:

- Complaints and service call data are considered when assessing the suitability of the Financial Products and Services offered to customers.

- Surveys assist to ensure that Financial Products and Services meet the needs and risk profiles of customers.

- When Financial Products and Services are designed, suitable customers are identified, and are aligned with the Company’s strategic objectives, business model, risk management, rules and regulations.

- Customers’ understanding of the Company’s offered Financial Products and Services is evaluated, and risks that the Financial Products and Services may pose to certain client groups are identified and mitigated.

- The Financial Products and Services selection and approval process includes Exco confirmation that the TCF outcomes have been suitably considered.

- Marketing, sales, and complaints are tracked to establish whether Financial Products and Services meet the needs of identified client groups and are targeted accordingly

7. Outcome 3: clear and appropriate information

7.1. The Company provides regular, clear, appropriate information and reports to its customers which

considers the needs and circumstances of customers.

7.2. Procedures implemented to achieve Outcome 3:

- Customers are informed in a timely way when important events or changes take place which may impact them.

- Reports are provided to customers, comprising clear and appropriate information, to enable them to make informed decisions.

- Risks, fees, costs, and charges relating to Financial Products and Services are clearly and appropriately disclosed to customers.

8. Outcome 4: financial advice

8.1. The Company aims to provide customers with financial advice that is suitable and considers the client’s specific circumstances, if and when advisory services are offered.

8.2. When/if offered, procedures will be implemented to achieve Outcome 4:

- Financial advice will be provided to customers by appointed representatives of the Company, which is an authorised financial services provider (FSP), in terms of the FAIS Act.

- The Company will ensure that its representatives comply with the FAIS fit and proper requirements and are appointed for the correct financial products for which they are providing financial advice to customers.

- Key individuals will sample review the financial advice provided by the representatives of the Company for whom they are responsible.

- Compliance officers will perform sample monitoring of the financial advice provided by representatives of the Company.

9. Outcome 5: performance and standards of financial products and service

9.1. The Company aims to ensure that financial products perform as they have led customers to expect and that the financial services that the Company provides is of an acceptable standard and as customers are led to expect.

9.2. Procedures implemented to achieve Outcome 5:

- Financial Products and Services offered by the Company are suitable, value for money, and aim to meet the financial objectives, needs, and risk profile of its customers.

- Specific risks of the financial products are identified, managed appropriately, and are disclosed to customers in an easy-to-understand way.

- Information about the financial products offered by the Company is provided to its customers in a transparent and easy to understand way.

10. Outcome 6: post-sale barriers

10.1. The Company aims to ensure that its customers do not face unreasonable post-sale barriers to

change financial products, switch product suppliers, switch financial services providers, submit a claim,

or make a complaint.

10.2. Procedures implemented to achieve Outcome 6:

- The Company proactively informs its customers of the types of changes they may make to their financial products if their financial objectives, needs, risk profile, or circumstances, change.

- The Company proactively informs its customers of important limitations on their ability to access their money within their financial products, or their ability to make changes.

- If/Where applicable, the appointed representatives of the Company provide customers with ongoing financial advice, with at least annual reviews performed, to keep updated with each client’s specific circumstances. Customers are informed about how to change financial products, switch product suppliers, switch financial services providers, submit claims, or make Complaints.

- If a client wants, or is recommended, to change an existing financial product, partially or wholly, the client is provided with all the differences between the financial products as well as the mandatory replacement record of advice (where advice is provided), which is also provided to the product suppliers, as prescribed by legislation.

- Customers are informed about the processes involved in changing financial products.

- If a client’s request to change a financial product is declined, the client is provided with clear reasons, therefore.

- The complaints process is detailed in a complaints policy and procedure, which is easy for customers to find, and all material reflects where customers can find the complaints policy and procedure

11. TCF Champion

11.1. The head of the Company has formally appointed Pinky Wisani as the TCF Champion, who is person responsible for implementing and maintaining the TCF standards within the Company and reporting same to the Head of Legal & Compliance, Peter Johnson.

11.2. The responsibilities of the TCF Champion include:

- To be actively involved in embedding the TCF principles into the Company’s business activities.

- To be actively involved in creating, and maintaining, a culture of treating customers fairly.

- To assist the Exco to implement and adopt business processes aimed to ensure that the Company is achieves the TCF outcomes.

- Having the authority to approach and speak to employees, regardless of hierarchy, about delivering and achieving the TCF outcomes.

11.3. The TCF Champion does not need to have specific qualifications but must have a reasonably thorough knowledge of the Company’s business areas, processes, and the principles associated with treating customers fairly.

12. Consequences of non-compliance with the policy

12.1. All employees are obliged to comply with the Policy and it is a condition of employment. Noncompliance is a breach of employment contract and is an action of misconduct, so employees may be subject to disciplinary action which may lead to dismissal. Non -compliance by an employee will be dealt with according to the Company’s disciplinary policy. For assessing and addressing the non-compliance, reports made by the compliance officers, internal audit, external audit, and the Authorities, will be considered, for appropriate action to be taken.

13. Policy review

13.1. The policy will be reviewed annually, updated, if necessary, and the latest version will be adopted and approved by the board.

Annexure A: Financial Products and Services, offered by the Company: